{kind=link}

{kind=link}

Walk into a gleaming dealership and everything whispers new beginnings. The paint reflects the lights like a calm lake at sunrise. The interior smells like promise. The dashboard screens glow with the confidence of modern engineering. For many people, buying a brand-new car feels like a milestone—proof that you’ve arrived, that your hard work has crystallized into something tangible, useful, and beautiful.

But once the emotional fog clears, a harder question rolls into view:

Is a brand-new car really a good investment?

This is not a simple yes-or-no question. It lives at the intersection of finance, psychology, technology, and lifestyle. To answer it properly, we need to redefine what “investment” means, examine how cars actually behave over time, and separate emotional satisfaction from financial reality. We also need to look at modern shifts—electric vehicles, software-driven features, subscription models, and changing ownership habits—that complicate old assumptions.

This article takes a clear-eyed, professional, and practical look at the topic. No hype, no citations, no sales pitch—just reasoning, examples, and structured thinking. By the end, you should be able to decide whether buying a brand-new car makes sense for you, not just in theory.

1. What Do We Mean by “Investment”?

Before judging whether a new car is a good investment, we need to define the word itself. In finance, an investment typically has three core characteristics:

- Capital outlay today

- Expected future returns

- Potential appreciation or income generation

Stocks, bonds, real estate, and businesses fit this definition well. They may fluctuate, but they are purchased with the expectation that they will either produce income or increase in value over time.

A car, however, occupies a different category.

For most people, a car is a consumable durable good, not a financial asset. It is purchased primarily for utility—transportation, convenience, independence—not for profit.

So when people ask whether a new car is a “good investment,” they are often asking one of three slightly different questions:

- Is it financially smart compared to alternatives?

- Does it hold its value well?

- Does it improve my life enough to justify the cost?

These are valid questions, but they are not the same as asking whether a car will make you money. With that distinction in mind, we can move forward honestly.

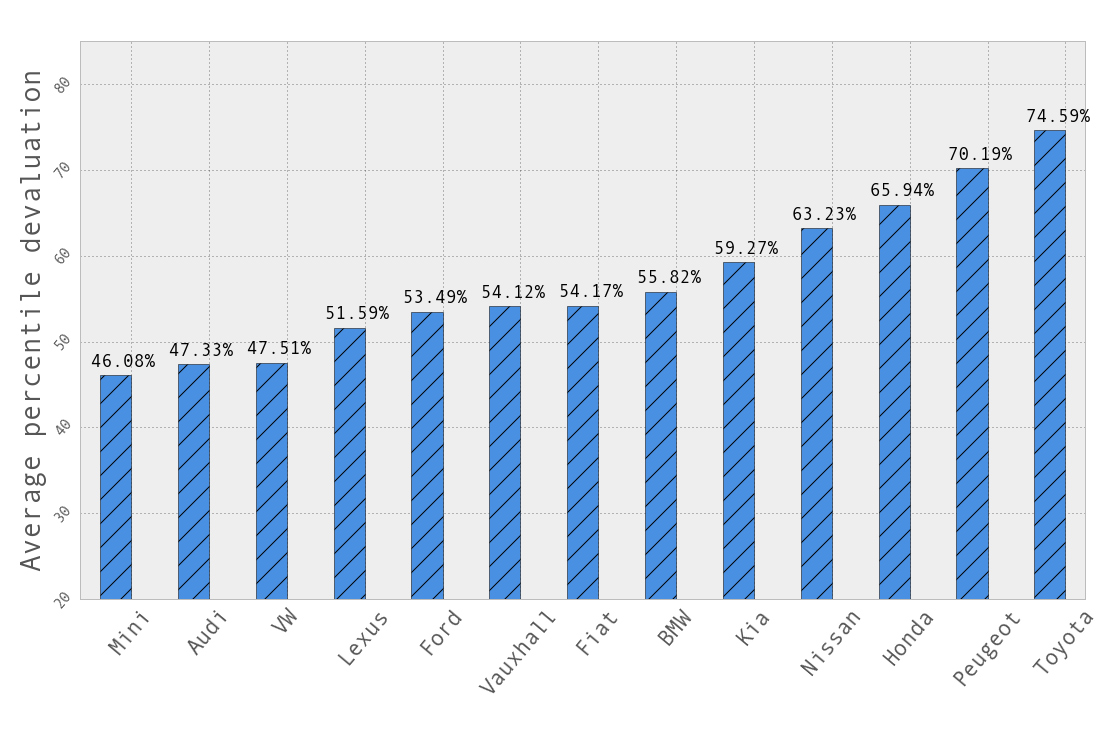

2. The Cold Reality: Depreciation Starts Immediately

The moment a brand-new car leaves the dealership lot, something dramatic happens: its market value drops.

This phenomenon is so well-known that it has become a cliché, but clichés exist because they are true. On average, a new car loses a significant portion of its value within the first year of ownership. Over the next several years, the decline continues, though at a slower pace.

Why does this happen?

2.1 The “New” Premium

A new car carries a premium for:

- Zero prior ownership

- Untouched mechanical components

- The latest features

- Manufacturer warranties

- Psychological satisfaction

Once the car is no longer new, that premium evaporates. Even if the car has only a handful of miles, the market treats it differently.

2.2 Rapid Model Cycles

Manufacturers release updates frequently:

- Facelifts

- Technology refreshes

- Improved fuel efficiency

- New safety systems

Each update nudges older versions downward in perceived value. Your car doesn’t become worse—but newer ones make it look worse by comparison.

2.3 Market Abundance

Cars are mass-produced. Unlike rare collectibles or limited assets, most vehicles exist in huge numbers. Abundance suppresses long-term value.

From a strict financial perspective, depreciation alone is enough to disqualify most brand-new cars as “investments” in the traditional sense.

But depreciation is only part of the story.

3. The Hidden Costs of Ownership

When people calculate the cost of a new car, they often focus on the purchase price or monthly payment. This is a mistake. The real cost of ownership is broader and more subtle.

3.1 Financing and Opportunity Cost

If you pay cash for a new car, you lock a large amount of capital into an asset that declines in value. That money could have been:

- Invested

- Used to reduce high-interest debt

- Reserved for emergencies

- Deployed into education or business

If you finance the car, you add interest payments to the total cost. Even at low interest rates, the effect compounds over time.

In both cases, there is an opportunity cost—the cost of what your money could have done instead.

3.2 Insurance Premiums

New cars generally require comprehensive insurance coverage, which is more expensive than basic policies. Advanced technology, sensors, and materials also increase repair costs, which insurers pass on to you.

3.3 Taxes, Fees, and Registration

Sales taxes, registration fees, and other administrative costs hit hardest at the point of purchase—and they scale with vehicle value. A more expensive new car brings proportionally higher ongoing fees.

3.4 Maintenance: Lower, Then Higher

New cars usually enjoy a honeymoon period:

- Minimal maintenance

- Warranty coverage

- Fewer unexpected repairs

However, once warranties expire, maintenance costs rise. Advanced features can also make repairs more specialized and expensive than older, simpler vehicles.

None of these costs are inherently bad. But they all count against the idea of a new car as a strong financial choice.

4. The Emotional Dividend: A Value That Doesn’t Show on Spreadsheets

Now let’s address the part that financial models struggle to quantify: how a new car makes you feel.

Humans do not live in spreadsheets. We live in stories, routines, and emotions.

4.1 Reliability and Peace of Mind

For many people, reliability is priceless. A new car offers:

- Fewer breakdowns

- Predictable performance

- Manufacturer support

If your livelihood depends on transportation, avoiding downtime can be more valuable than squeezing out maximum financial efficiency.

4.2 Confidence and Comfort

Modern cars offer:

- Advanced safety systems

- Better ergonomics

- Quieter cabins

- Smarter interfaces

These features can reduce stress, fatigue, and anxiety—especially for long commutes or family travel.

4.3 Identity and Motivation

Cars are personal. They reflect taste, priorities, and sometimes success. For some buyers, a new car serves as:

- A reward

- A motivator

- A symbol of progress

While these benefits are subjective, they are real. Ignoring them leads to incomplete analysis.

The key question is not whether emotional value exists—but whether it justifies the financial trade-off in your situation.

5. When a Brand-New Car Can Make Sense

Although a new car is rarely a financial investment, there are scenarios where buying new is rational and defensible.

5.1 Long-Term Ownership

If you plan to keep the car for a long time—well beyond the steepest depreciation period—the initial value loss becomes less relevant. Over ten or more years, the cost difference between new and lightly used narrows.

In this case, buying new allows you to:

- Control the entire maintenance history

- Avoid unknown wear and abuse

- Choose exact specifications

5.2 Specialized Needs

Certain use cases benefit from buying new:

- Vehicles with specific configurations

- Commercial or professional use

- New technology adoption (such as early electric platforms)

When precision matters, the flexibility of ordering new can outweigh the cost.

5.3 Manufacturer Incentives

Occasionally, manufacturers offer:

- Warranty extensions

- Service packages

- Favorable financing

- Trade-in bonuses

These incentives can reduce the effective cost gap between new and used, especially when paired with careful negotiation.

5.4 Safety and Technology Priorities

Safety technology evolves quickly. For families or high-mileage drivers, access to the latest systems can be a legitimate priority rather than a luxury.

In these cases, the question shifts from “Is this an investment?” to “Is this the most efficient way to meet my needs?”

6. The Used Car Comparison: Why It Often Wins Financially

Used cars are often praised as the smarter financial choice—and with good reason.

6.1 Depreciation Advantage

By purchasing a car after the initial depreciation hit, you let someone else absorb the largest value loss. This single factor can dramatically improve cost efficiency.

6.2 Similar Utility, Lower Cost

A well-maintained used car can deliver nearly the same functionality as a new one:

- Comparable performance

- Adequate safety

- Familiar technology

For many drivers, the difference in daily experience is smaller than expected.

6.3 Broader Market Flexibility

The used market offers:

- More pricing variability

- Greater negotiation leverage

- Access to higher-tier models at lower prices

From a purely financial standpoint, used cars often provide more “transportation per dollar.”

That said, used cars also come with risks—unknown history, limited warranties, and potential maintenance surprises. The best choice depends on your tolerance for uncertainty.

7. The Rise of Electric and Software-Driven Cars

Modern vehicles are no longer just mechanical machines. They are rolling computers, and this shift complicates the investment question.

7.1 Rapid Obsolescence

Software evolves faster than hardware. Features that feel cutting-edge today may seem outdated in a few years. Over-the-air updates help, but not all improvements are backward-compatible.

7.2 Battery Degradation Concerns

For electric vehicles, battery health plays a central role in long-term value. While technology continues to improve, uncertainty remains a factor that affects resale and ownership confidence.

7.3 Subscription Models

Some manufacturers now lock features behind software subscriptions. This introduces ongoing costs and blurs the line between ownership and access.

In this environment, buying new does not guarantee long-term relevance. In fact, it may expose you more directly to rapid technological change.

8. Cars as Lifestyle Tools, Not Financial Assets

Perhaps the most productive way to think about a new car is not as an investment—but as a tool.

Like:

- A high-quality mattress

- Professional equipment

- Reliable home appliances

These items are not purchased to grow wealth, but to support daily life efficiently and comfortably.

When framed this way, the question becomes clearer:

Does this car deliver enough value, reliability, and satisfaction to justify its total cost over time?

If the answer is yes, the purchase can be considered successful, even if it never makes financial sense on paper.

9. Common Psychological Traps to Avoid

When evaluating a new car purchase, watch out for these mental shortcuts:

9.1 Monthly Payment Illusion

Low monthly payments can mask high total costs, especially with long loan terms.

9.2 Feature Overvaluation

Paying extra for features you rarely use erodes value faster than you expect.

9.3 Social Comparison

Buying to match others’ expectations rather than your own needs often leads to regret.

Awareness is the best defense against these traps.

10. A Smarter Decision Framework

Instead of asking whether a new car is a good investment, ask these questions:

- How long will I keep this car?

- How critical is reliability to my daily life?

- What alternatives exist at lower cost?

- What am I giving up financially to buy this?

- How much emotional value does this bring me?

Answering honestly leads to better outcomes than any generic rule.

11. Final Verdict: Investment or Indulgence?

So, is a brand-new car really a good investment?

Financially? Almost never.

Practically? Sometimes.

Emotionally? Often.

A brand-new car is best understood as a controlled indulgence—one that trades future financial efficiency for present comfort, reliability, and satisfaction. When chosen deliberately and aligned with long-term plans, it can be a rational and rewarding purchase.

But if the goal is wealth creation, cars—especially new ones—are the wrong battlefield.

The smartest buyers are not those who avoid new cars entirely, but those who understand exactly what they are buying: not an asset that grows, but a machine that supports life as it moves forward.